Insights - June 2026

The market is changing quickly after three rate rises, major Budget reforms and rising fuel prices. Here are four developments that could influence your next financial decision:

In regard to the Tasmanian Budget, there has been some changes affecting first home buyers.

Unfortunately, he First Home buyers grant for new homes has been reduced to $20,000. Also the 100% stamp duty rebate for established homes has been removed.

In this issue, we look at:

Budget tax changes reshape property investing

Could interest-only reduce repayment pressure?

Why housing supply remains tight

EV sales hit another record high

Keep reading for all the news.

Property investors are weighing up their next move after the federal Budget unveiled sweeping changes to property tax rules.

The proposed reforms would:

Limit negative gearing on residential properties to new builds.

Replace the 50% capital gains tax discount with inflation indexation.

Introduce a 30% minimum tax rate on capital gains.

Most changes would start from 1 July 2027.

Why current owners may see little immediate impact

The reforms would largely ‘grandfather’ existing properties.

If you already own an investment property purchased before the 12 May 2026 announcement, you’ll still be able to negatively gear it in future years.

That transitional arrangement is designed to reduce disruption and avoid a rush of buying or selling.

What buyers may do differently

If the reforms proceed, future investors may increasingly focus on:

Newly built homes.

Properties that add housing supply.

Longer-term hold strategies.

At the same time, some buyers may reassess whether property still suits their goals compared to other investments.

Why structure matters now

This isn’t just a tax story – it’s also a finance story.

Loan structure, cash flow and borrowing strategy could become even more important if tax settings change.

I can help you understand how lenders may assess investment scenarios under the proposed rules and what options may suit your plans.

After three rate rises in 2026, some borrowers are looking beyond refinancing and reconsidering how their mortgage is set up.

The Reserve Bank has increased the cash rate by a total of 0.75 percentage points this year, and most lenders have passed those increases through to variable-rate customers.

As repayments rise, borrowers are exploring different ways to manage cash flow.

One option gaining attention

Some borrowers are considering switching from principal-and-interest repayments to interest-only repayments.

That can reduce monthly repayments in the short term because you’re temporarily paying only the interest, not the loan principal, although repayments are higher over the life of the loan.

Why interest-only isn’t for everyone

Interest-only can improve flexibility during periods of higher costs or reduced income.

But there are downsides:

The loan balance doesn’t reduce during the interest-only period.

Repayments can jump later when principal repayments resume.

Lenders may charge higher interest rates for interest-only loans.

That means it’s usually more of a short-term strategy than a permanent solution.

Why borrowers are planning ahead

With rates potentially rising further, many borrowers are now stress-testing their budget rather than assuming conditions will quickly improve.

That includes reviewing:

Loan structure.

Repayment buffers.

Offset balances.

Fixed versus variable options.

I can help you understand the pros and cons of different loan structures and assess what may suit your situation in the current environment.

Review your mortgage structure

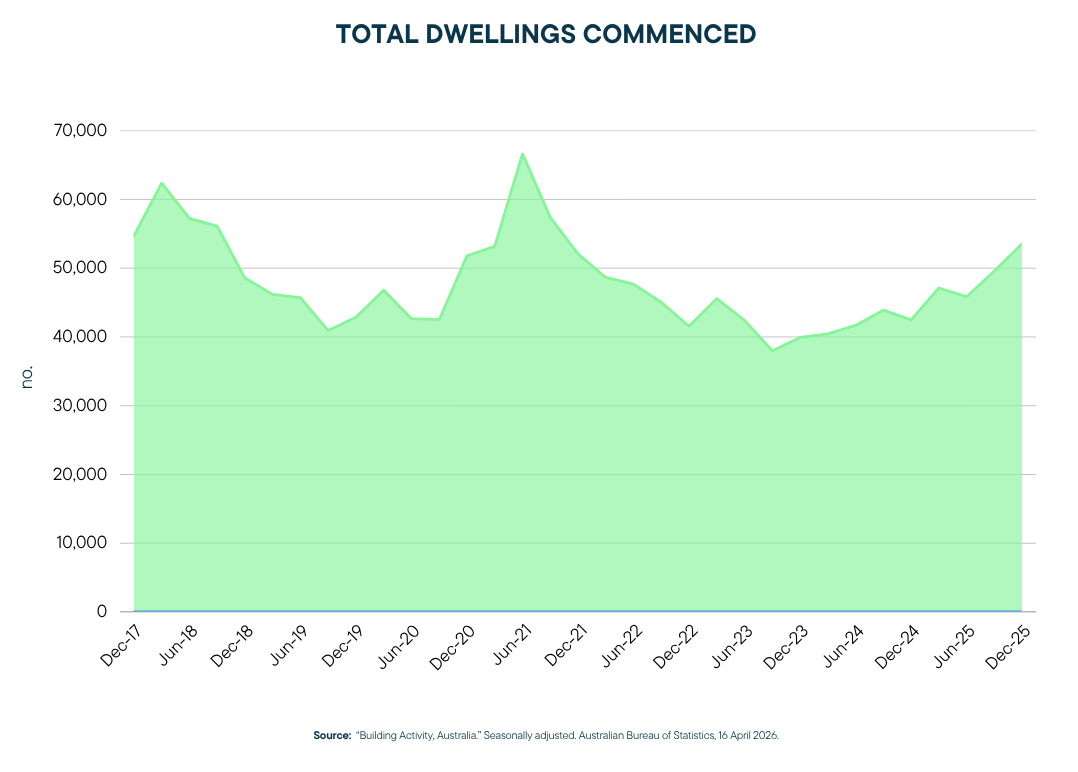

Home construction is increasing, but Australia is still falling well short of the housing needed to meet future demand.

According to the ABS, construction started on 196,118 homes in 2025, up from 168,492 in 2024.

That’s a meaningful improvement.

But it also highlights how difficult it will be to achieve the federal government’s target of facilitating the construction of 1.2 million new homes by June 2029.

Why supply remains a challenge

Builders and developers are still dealing with:

Labour shortages.

High construction costs.

Planning delays.

Infrastructure constraints.

In many locations, new housing projects can’t proceed because roads, sewerage, water and power connections aren’t ready.

The government’s latest response

In the recent Budget, the federal government announced a new $2 billion Local Infrastructure Fund.

The funding is designed to help councils and utilities deliver the “last mile” infrastructure needed to support new housing developments.

The government says the program could support up to 65,000 homes over the next decade.

States and territories will only receive funding if they commit to reforms such as:

Speeding up approvals.

Making more land available.

Simplifying building rules.

Why buyers should pay attention

Housing supply has become one of the biggest influences on long-term affordability.

If supply remains constrained while population growth continues, that could continue placing pressure on prices and rents over time.

Electric vehicles are becoming increasingly mainstream, with rising fuel costs and government incentives driving stronger demand.

According to the Federal Chamber of Automotive Industries, EVs accounted for a record 16.4% of all new vehicle sales in April.

That follows a steady increase in EV supply since the introduction of the New Vehicle Efficiency Standard, alongside higher petrol prices and ongoing tax incentives.

What’s changing with EV incentives

In the recent Budget, the federal government announced changes to the Electric Car Discount.

Under the new arrangements:

Eligible EVs costing up to $75,000 will continue receiving a full fringe benefits tax exemption if the arrangement begins before 1 April 2029.

Eligible EVs above $75,000 will move to a permanent 25% FBT discount from 1 April 2027.

All eligible EVs will move to the 25% discount model from 1 April 2029.

Importantly, existing arrangements will not be affected.

Why buyers are paying attention

For many households, the focus is shifting beyond purchase price. Buyers are increasingly weighing up fuel savings, running costs, tax benefits and long-term affordability.

As EV options continue expanding, more buyers are weighing up whether switching now makes financial sense.

I can help you understand the finance options available and structure a vehicle loan that fits your budget and plans.

Explore your vehicle finance options

As borrowers adapt to higher rates and investors rethink property strategy, planning ahead matters more than ever. If you’d like to explore your options, reach out and we’ll work through them together.

Kind Regards,

AllanFaint

Contact Us

Home Finance Centres Of Australia

NAB Building, unit 1, level 2, 86Collins St.

HobartTAS7000

Australian Credit License Number 390540

Disclaimer:The information provided above is on the understanding that it is for illustrative and discussion purposes only. Any party seeking to rely on its content or otherwise should make their own enquiries and research to ensure its relevance to your specific personal and business requirements and circumstances.

Resources: Article two:reference oneArticle two:reference oneArticle three:reference one,reference two,reference three, reference fourArticle four:reference one,reference two

This email was sent to. Don't want to receive these anymore?Unsubscribe here.

Powered byActivePipe, aMoxiWorksProduct